September 12, 2018

First of all, we would like to take a minute to remember all those that lost their lives some 17 years ago today. We will remember that day for quite some time, in fact it was on this day, a sunny crisp Tuesday morning that our phone lines went down to our trading partners inside One World Trade Center at Cantor Fitzgerald. We knew right there and then that something was up and we watched it unfold right before our eyes. Being on the floor of the CBOT, we evacuated and left the city for fear that we might be targeted next. We will never forget those and their families that were so tragically affected that fateful day and we will acknowledge their memorial this time every year for as long as we can.

There’s a lot to get to, but first we would like to thank Anthony Crudele and the crew at Futures Radio Show for allowing us the opportunity to talk about our views on the markets and trading. The link to the show can be found HERE

We also want to thank Greg Winterton at AlphaWeek for the great article they put out this week. He is the founder of AlphaWeek an informative and vast resource for every investor. The link to the article about Magnelibra and the Blue Dragon Program can be found HERE.

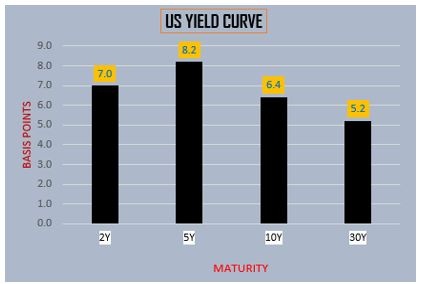

So, the obvious news last week was the non-farms payroll report which put in a respectable +201k which beat expectations mildly, however both June and July were revised down a combined total of 50k jobs. The larger and more inflationary issue arose as the YoY growth in avg. hourly earnings hit 2.9%. US treasuries took exception and felt the FED would continue their hiking ways and yields rose. As you can see from this chart of the US Yield Curve from Friday’s settles, shorter dated yields rose higher in comparison to their longer end counterparts:

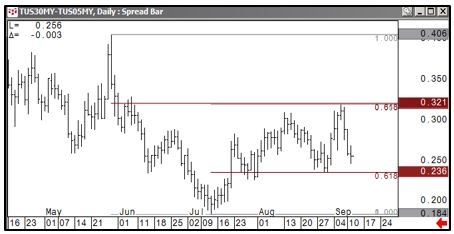

Here is a chart of the US 5s30 curve chart courtesy of D.Wienke of Cabrera Capital:

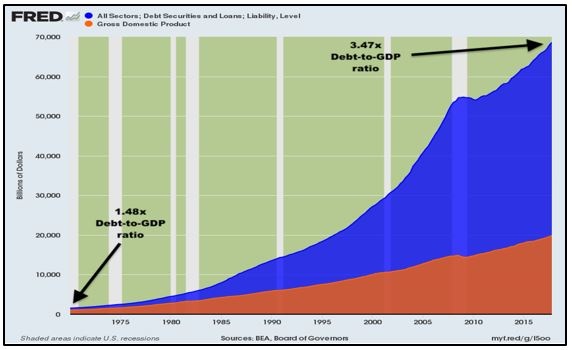

We also read a great piece from Adam Taggart via PeakProsperity.com and also found on Zhedge. Adam posted a chart that really encapsulates how America’s growth has been driven via debt and not organic savings and investment. What is worse is that the debt/growth regime is subject to the laws of mathematics and diminishing returns. It takes increasingly more debt to generate $1 in GDP return. Countries can get away with this for a little while but you can guess why shorter interest rates are truly still zero. In the land of mathematics, you can’t have your debt issuing cake and eat your interest too, there are limits. Meaning we can keep the debt train rolling, but eventually the debt service payments will overwhelm your regime, and it’s not a matter of if but when, can you say $1 Trillion-dollar deficits:

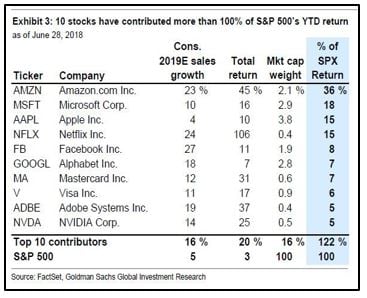

Zhedge also had a piece from Nomura posting this chart, which if it isn’t obvious by now, just a very few securities are pulling all the weight. What happened to all that Chicago U. Efficient Market Hypothesis, is this what they had in mind? 4 companies accounting for 84% of all the SP500 market returns? As this next chart points out 10 stocks have contributed to 100% of the return so far this year:

Let’s take a look at some tech charts before we get to other news, first up speaking of the FAANGs they are holding up the markets for now and have bounced off supports:

The SPY still resides in its 7-month trend channel, but we are concerned:

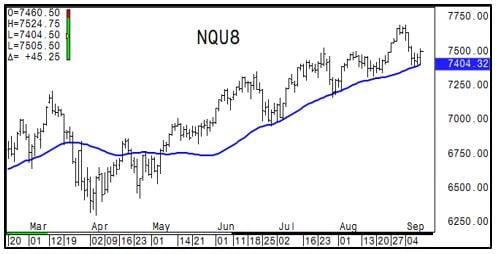

The Nasdaq has seen obvious buying here, and stops should be obvious as well:

As far as the US bond future it’s had quite some trouble near 146 and continues to hold a 2-year long support level near 140-00, we feel that above/below those levels will usher in new trading parameters, but chop in between expected for now:

Crude oil continues to be this year’s top performer, swapping that title with the Nasdaq, but the chart has been stagnant lately with renewed selling most likely with a move below $66:

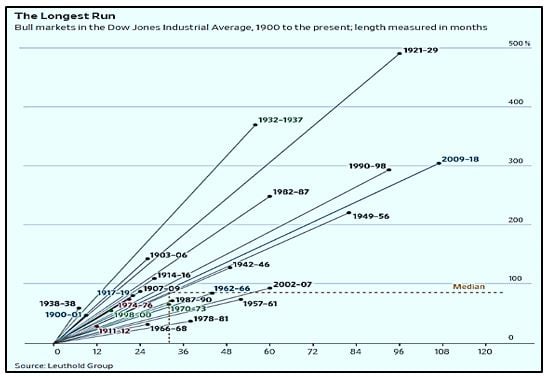

So, when we spotted this chart in the WSJ something stood out to us, this current bull market maybe the longest, but it’s not the most in % return, in fact its barely 3rd. We can’t fathom the obvious central bank debt load that has been created in order to achieve this feat, but it sure is interesting to note that we’ve racked up all this debt and this is the best we can do? Then again, if it’s all just predicated on debt growth, then how truly stable is it?

Ok, so what else did we read last week? The WSJ had a great article on the Cboe planning to implement a “speed bump” to try and level the HFT playing field. We are a big fan of such constructs and believe that the field is plagued by predatory latency arbs.

In another interesting article, highlighted the ongoing battle between a new bank called TNB USA, run by a former NY FED staffer no less, is suing the NY FED for unfairly preventing them to pursue their business model. Which isn’t a noteworthy or feat of any genius, rather its design is simple, it’s an interest rate arb, that will exploit the guaranteed IOER upper limit that is only available to those with a Fed account. We doubt that TNB will win this case, for fear of precedent and the Federal Reserve is quite formidable to say the least, but good luck.

In a lighter note, we read that none other than Burberry is disavowing their practice of wastefully burning excess inventory, which was reportedly valued just short of £30 million Pounds last year. We first highlighted this practice in a note a few months back, one which certainly does not stick with the so called “green” initiative. We wonder how this will affect their brand and whether or not some will opt to wait for excess supply to be discounted as opposed to paying full price. In economics we studied this practice and in fact it is very effective at protecting brand value, we just aren’t sure if this is a change in their ways or just a temporary “saving face.”

Not helping Ford Motor company’s shares this week and which are already down some 24% this year, is a recall effecting 2 million F-150 models. This comes at a time where Ford is eliminating most of their sedan models and opting to focus their core production fleet on trucks. We aren’t quite sold on that move, but maybe it’s a way to hide the fact they are streamlining production and ops in order to enact much needed cost cuts.

Finally, we would like to congratulate Naomi Osaka on her win over her childhood inspiration Serena Williams at the US Open. Serena didn’t take it very well, but we understand her frustration in such a situation, however we don’t respect the politicization of her anger. We would have respected it more if she just acted like the champion she is. On the other side of the court Novak Djokovic won his 3rd US Open which comes after an impressive recovery from surgery earlier this year. Before we forget and for our readers who have teenagers, the WSJ put out an awesome piece on GenZ. With a total of some 67 million they will be a force over the next two decades and the article did a great job of outlining some of their attributes, where surveys have shown that Gen Z members are socially cautious while being focused on work and financial security, well worth the read.

Our condolences to the family of Burt Reynolds, the Hollywood Icon who died last Thursday at the age of 82. We didn’t know he had a football scholarship to play for the Seminoles of FSU, but instead decided to go into acting, Smokey and the Bandit, Deliverance, The Longest Yard, #Classics.

Our condolences to the family of Burt Reynolds, the Hollywood Icon who died last Thursday at the age of 82. We didn’t know he had a football scholarship to play for the Seminoles of FSU, but instead decided to go into acting, Smokey and the Bandit, Deliverance, The Longest Yard, #Classics.

Speaking of classics, the NFL kicked off this weekend and it was Green Bay and The Bears on Sunday Night Football and what looked to be a surprising blow out by the Bears after the first half. However true to form, The Bad News Bears found a way to lose, then again Aaron Rodgers is well, Aaron Rodgers. The highest paid defenseman in the league didn’t disappoint, but you know what they say, personal accolades are great but, “winning is everything” and in professional sports if you don’t win, well, nothing else matters!

Speaking of classics, the NFL kicked off this weekend and it was Green Bay and The Bears on Sunday Night Football and what looked to be a surprising blow out by the Bears after the first half. However true to form, The Bad News Bears found a way to lose, then again Aaron Rodgers is well, Aaron Rodgers. The highest paid defenseman in the league didn’t disappoint, but you know what they say, personal accolades are great but, “winning is everything” and in professional sports if you don’t win, well, nothing else matters!

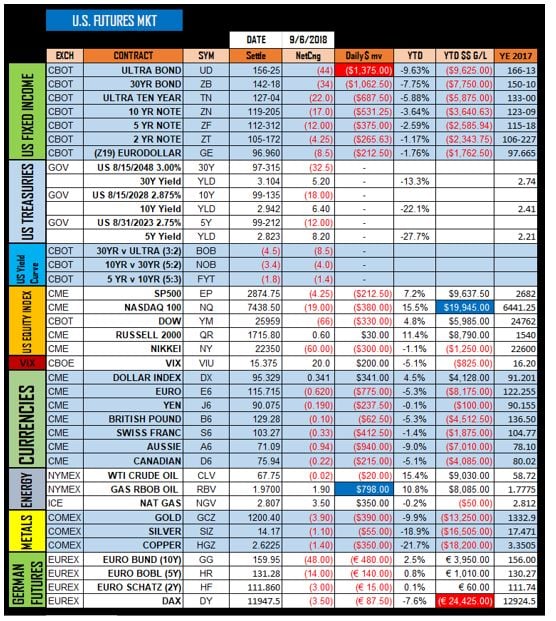

September 7th Futures settles below:

Finally, we will decidedly end our notes with our reaffirmation of the growing need for alternative strategies. We would like to think that our alternative view on markets is consistent with our preference for alternative risk and alpha driven strategies. Alternatives offer the investor a unique opportunity at non correlated returns and overall risk diversification. We believe combining traditional strategies with an alternative solution gives an investor a well-rounded approach to managing their long term portfolio. With the growing concentration of risk involved in passive index funds, with newly created artificial intelligence led investing and overall market illiquidity in times of market stress, alternatives can offset some of these risks.

It is our goal to keep you abreast of all the growing market risks as well as keep you aligned with potential alternative strategies to combat such risks. We hope you stay the course with us, ask more questions and become accustomed to looking at the markets from the same scope we do. Feel free to point out any inconsistencies, any questions that relate to the topics we talk about or even suggest certain markets that you may want more color upon.

____________________________________________________________________________________

Capital Trading Group, LLLP ("CTG") is an investment firm that believes safety and trust are the two most sought after attributes among investors and money managers alike. For over 30 years we have built our business and reputation in efforts to mitigate risk through diversification. We forge long-term relationships with both investors and money managers otherwise known as Commodity Trading Advisors (CTAs).

We are a firm with an important distinction: It is our belief that building strong relationships require more than offering a well-rounded set of investment vehicles; a first-hand understanding of the instruments and the organization behind those instruments is needed as well.

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

This newsletter is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete. It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.