October 11, 2021

Why implied volatility is a critical tool for all traders & investors.

By Andrew Hecht

- The past is history; the present is all that matters for traders and investors

- Historical volatility is a map of the past price variance for asset prices

- Implied volatility is a real-time sentiment indicator

- The primary variable determining put and call option prices

- The three critical factors implied volatility reveals

Perception is a way of regarding, understanding or interpreting something. Through the perceptual process, we gain information about the properties and elements of the environment that are critical to our survival.

Traders and investors use different sets of tools when approaching markets. Some are fundamentalists, pouring through balance sheets, supply and demand data, and other macro and microeconomic information to predict the future prices of assets. Others have a strictly technical approach to markets, following trends and the path of least resistance of prices. Still, others combine the two to look for opportunities where fundamental and technical analysis merge to improve the chances of success.

Yogi Berra, the hall of fame catcher and armchair philosopher, once said, “The future ain’t what it used to be.” All market participants have the same goal, to increase their nest eggs. Projecting the future is the route to achieve their goal.

Implied volatility is a tool that all market participants need to embrace as it is a real-time indicator of market sentiment.

The past is history; the present is all that matters for traders and investors

History depends on interpretation. When it comes to markets, Napoleon Bonaparte may have said it best, “history is a set of lies agreed upon.” An asset’s price moved higher or lower in the past because of a collection of variables viewed through a prism that leads to a collective conclusion that has broad acceptance but may not be accurate. Taking a risk based on an inaccurate conclusion could lead to mistakes and losses.

When we consider buying or selling any asset, all that matters is the present. The current price of any asset is always the correct price because it is the level a seller is willing to accept and a buyer is willing to pay in a transparent environment, the market.

Historical volatility is a map of the past price variance for asset prices

Historical volatility is an objective statistical tool that defines the price variance of the past. Any disclosure document tells us that past performance is no guaranty of future performance. We must view historical volatility precisely the same way, with more than a grain of salt.

Historical volatility is a guide, but remember what Yogi said, “the future ain’t what it used to be!”

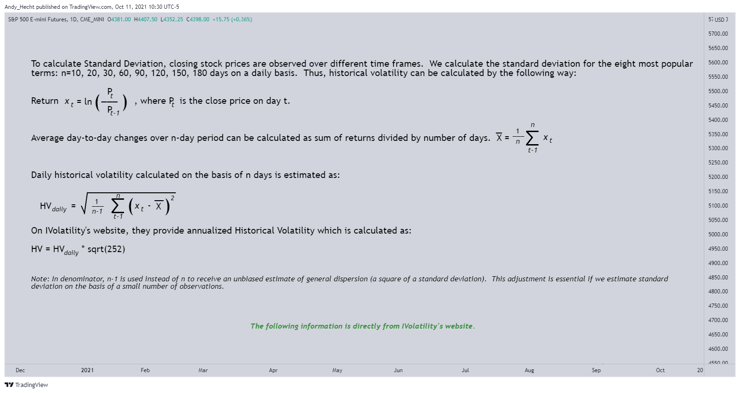

We calculate historical volatility by determining the average deviation from the average price over a given period. When it comes to math, the formulas are:

Source: IVolatility

A simple explanation of the complicated formula comes in seven easy steps:

1. Collect the historical prices for the asset

2. Compute the expected price (mean) of the historical prices.

3. Work out the difference between the average price and each price in the series.

4. Square the differences from the previous step.

5. Determine the sum of the squared differences.

6. Divide the differences by the total number of prices (find variance).

7. Compute the square root of the variance computed in the previous step.

Implied volatility is a real-time sentiment indicator

While we can calculate historical volatility from historical data, implied volatility is a different story. Implied volatility is the expected or projected volatility or price variance of an asset over time.

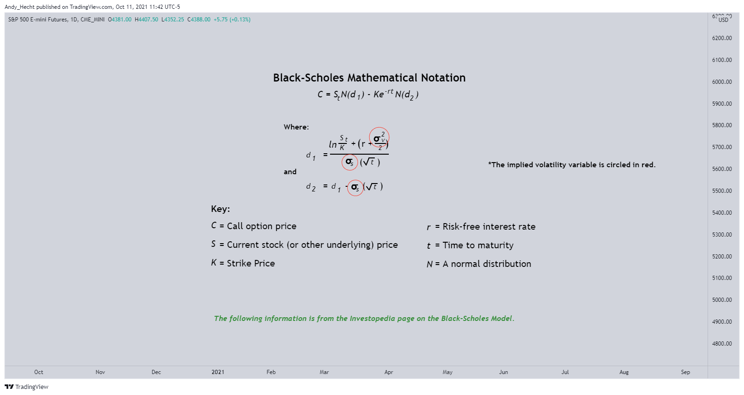

We back into calculating implied volatility using an options pricing model. We can establish an implied volatility reading by entering the option value into the Black-Scholes options pricing formula or other formulas that determine options prices. If we have a put or call options price, we can solve for the implied volatility level. The Black-Scholes formula in mathematical notation is:

Source: Investopedia

Source: Investopedia

The primary variable determining put and call option prices

There are no option prices without implied volatility as it is the critical variable that determines put and call option values. Yogi also said, “You can observe a lot by watching.” The current implied volatility level is the market’s consensus perception of what volatility or price variance will be during the life of the put or call option.

Observing and watching reveals the constant changes in implied volatility levels, which can be highly volatile over time. Option traders call an option’s sensitivity to changes in implied volatility Vega, which measures the change in an option price for a one-point change in implied volatility.

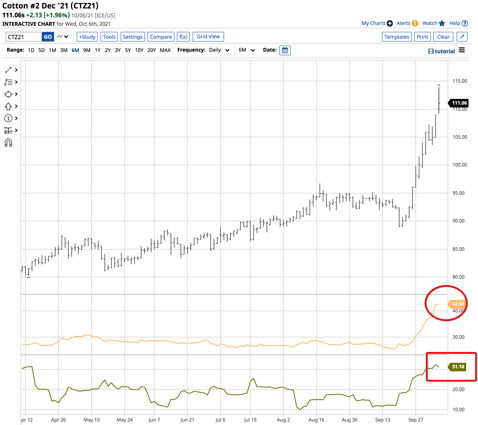

The cotton market recently took off to the moon in an explosive move.

Source: Barchart

Source: Barchart

The six-month chart of December ICE cotton futures shows that implied volatility stood around 42% (circled) on October 6 whole historical volatility was around 31% (squared). Implied volatility is the market’s perception of price variance; it tells us the collective wisdom believes cotton’s price will remain more volatile than the historical measure.

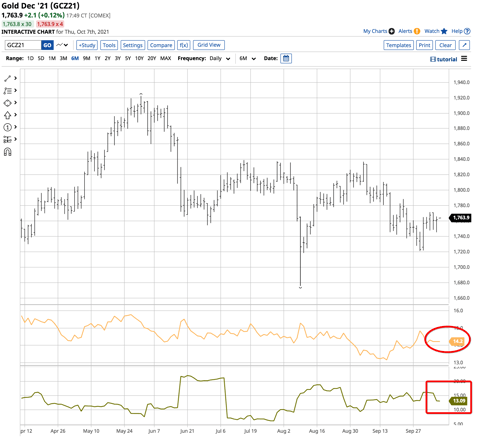

Gold is a sleepy market these days, with uninspiring price action for bulls and bears.

Source: Barchart

Source: Barchart

The spread between implied volatility at 14.2% and historical volatility at 13.09% is far narrower than in cotton. Gold’s implied volatility level tells us the market is not projecting any significant changes in gold’s price variance in the immediate future.

Implied volatility is constantly changing. Yogi had another great saying, “If the world were perfect, it wouldn’t be,” which rings true for implied volatility which can change in the blink of an eye. Option traders pay lots of attention to their Vega risk as the volatility of implied volatility can be…highly volatile! How’s that for a tongue twister?

The three critical factors implied volatility reveals

Implied volatility is a valuable tool for all traders and investors for three significant reasons:

- It is a real-time indicator of the market’s perception of the future price range of an asset.

- It can change suddenly, and changes often occur before the price of an asset reacts, making implied volatility a leading indicator.

- Implied volatility reflects the wisdom of the crowd, and crowds tend to make better decisions than individuals. Moreover, it is reading that reflects the present, not the past, and is a constantly changing measure of consensus forecasts for the future.

As traders and investors, we exist in the present. We attempt to increase our wealth with long and short risk positions that either add or subtract from our nest egg in the future. Implied volatility is a critical measure we should understand, utilize, and always keep in our toolbox. Any project requires the right tools. Implied volatility’s value is that it reflects a snapshot of the current market’s consensus.

Historical volatility depends on “Deja vu” happening “all over again.” Implied volatility is a measure that understands that the “future ain’t what it used to be.”

Trading advice given in this communication, if any, is based on information taken from trades and statistical services and other sources that we believe are reliable. The author does not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects the author’s good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice the author provides will result in profitable trades. There is risk of loss in all futures and options trading. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This article does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.