September 26, 2017

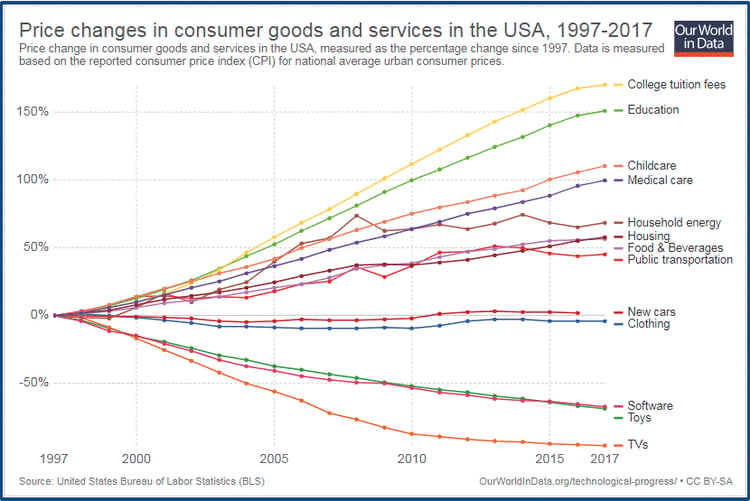

Last week saw an FOMC meeting that was widely anticipated as having no change to its interest rate policy and that was certainly the case. As for balance sheet reduction, that is to commence in October. The size and the scope of this rebalancing is not noteworthy because we truly figure the FED will merely adjust this as time moves to the left. Its miniscule to say the least and we really don't see it as having much of an overall impact as much as it seemed to be more of a credibility tool. Remember their balance sheet currently sits at some $4.4 Trillion so $5 billion a month in roll off, well you get the picture. One item that stood out and one that did a number on the short end of the yield curve was the fact that 12 members expect a rate hike in December, with just 4 expecting rates to remain unchanged. We suppose there was a little bit of everything for everyone as near term hawkishness was followed by longer term projections showing Fed Funds around 2.75%, couple that with their 2% inflation target, showing a benign growth projection. Speaking of inflation or lack thereof we have this juicy chart which we suppose, depending on your income bracket, the bottle may seem half full or half empty of inflation:

See this is where the real dilemma resides and one that we have touched upon many times in the past. Considering the QE bonanza over the last 9 years, we can't help but think all of this debt will one day have to be reckoned with and yeah it looks great for asset prices in the short term, but how are these levels sustainable in the long term? Have we not clearly sacrificed sustainable long term future economic growth, for short term economic asset price gains? Yes it's been a windfall for the top 1%, well actually the top 10% of the 1%. We get it, we know they control the assets, but how long can a paper gain be levered, be rehypothecated? Not everyone can be a saver, nor can everyone realize profits at the same time, we all know what happens. Needless to say, we will be quite intrigued to watch this one play out over the course of the next few years. We know that amongst internal domestic US conflict, global geopolitical conflict and block chain technology, these are just a few of the disruptors that are on our radar. Seems like these types of variables aren't easily quantified, and yet economic models continue to rely on static inputs that lack the variability that can only capture the real chaos of economic fundamentals.

So technically the damage to the US yield curve was done, but as we will show in our technical charts later on, equity market nervousness and NK tensions seemed to put a bid into bonds at week's end, to at least cover a bit of that short end selling.

When we speak of valuations and the ability for organic economic growth to sustain such lofty levels, we have this chart from Jared Dillan @dailydirtnap:

It shouldn't be much of a surprise considering the scope of monetary printing over the last decade, coupled with zero and even negative rates, but on a historical basis, it does capture the essence of what both bonds and equities are up against moving forward.

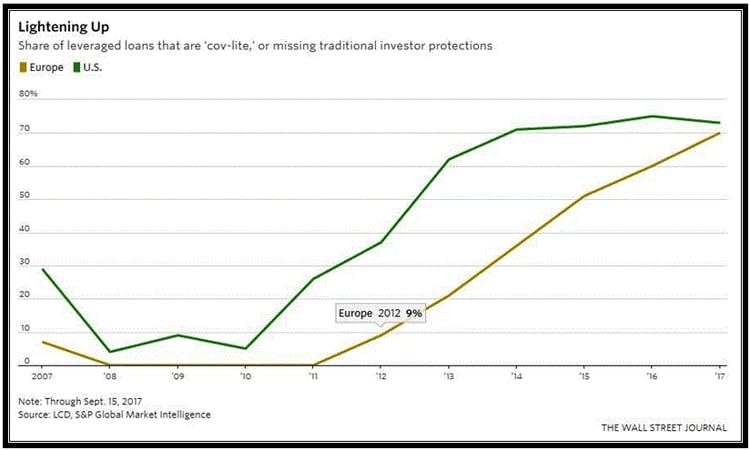

What should also not come to be a surprise is this next chart. Levered loans have been on a tear the last few years as everybody and anybody close enough to the monetary spigot has tried desperately to supercharge their yield enhancement given low levels of actual real yields out there. The way to do this is to obviously put up a certain amount of collateral and borrow, 4x, 5x, 6x and put it to work. Things look bright and shiny when asset prices rise and everyone piles in just to keep pace, but what happens when things turn? Leverage has a way of enticing then slicing its abuser without remorse. This chart shows the amount of "cov-lite" (little investor protection) bonds over the past few years being ramped up and slowly stagnating. Does this mean a few names are getting a bit nervous as to the overzealousness?

History doesn't repeat but it sure does rhyme and there are a few of us who have forged on over the last two decades to remember, nothing lasts forever. Kind of reminds of us a conversation from one of our favorite fictional characters, Bud Fox (Wall Street 1987) His manager says to him, "You're on a roll kid, enjoy it while it lasts, because it never does!"

We hate to think of how all these 20 something and even 30 something managers having never seen a bear market, how they will handle a down turn. They have spent the last decade riding a linear FED tsunami that, hasn't broke yet. We aren't saying if when and where the music will stop, but merely, stating that the odds as time moves to the left increase that likelihood significantly. With this last chart in mind, we figure large managers are going to begin to pay heavy attention to those IG and HY spreads once again. We should be putting on our radar the CDS of the most heavy abusers of the debt to equity swap to raise share prices over the last decade. As we stated before, leverage works both ways, and in fact even faster on the way down, so keep these things in mind. In fact UBS has a piece out just this week on the very subject of credit spreads and potential widening due to the FEDs change of hawkish heart.

Ok to other news, we have been hearing Apple's been telling suppliers to slow down on the components. Analysts are smart to comb supplier bases for future guidance and it's all a part of the new data collection in real time, to enhance forward guidance. Technology does have its limits and even the mighty Apple may have found that dreaded price ceiling for its product. We have talked a bit in the past about Apple having to keep ahead of the pack, we have seen this before, the high tech arena shows no mercy even if you have been accustomed to fantastic brand loyalty. Tech millennial's are finicky and given that Apple spends some $10 billion a year on R & D, superior products better continue or sales slumps won't take long to hit the bottom line. Yea they have a mighty war chest, which is why we believe growth through acquisition is inevitable. We aren't advocating its peak Apple season just yet, but hey it is what it is. By the way how many people can actually afford a $1k cell phone? Maybe that's the new securitized product, lets package a bunch of cell phone leases, we are sure it’s a growing business! One bright spot for Apple is that they are getting some backlash from the advertising industry about their new Safari update. This update limits advertiser/users tracking and closes prior loopholes. Advertisers are claiming that it's "destroying the economic model of the internet." Really? We didn't know the internet was created to make money? We just assumed it was for the direct and instantaneous ease of P2P communications and information delivery, call us old fashioned but no you are not entitled to anything! Anyhow, to read further if it interests you, Andres Arrieta wrote a great piece, "Apple does right by users and advertisers are displeased."

Moving to the geopolitical front, we have continued North Korean rhetoric, one which we feel is purely just that and nothing more. Markets will become anesthetized and this will continue to diminish unless something truly happens, which we hope is not the case. We favor diplomacy and peace above all else. Also out on Twitter is Russia claiming the US SPFs were out near ISIS positions in Syria and thus we have to continue to monitor this as to any effect in may have on our markets should things begin to escalate there as well. This is all a part of that geopolitical wild card nobody can truly quantify.

On the domestic front, we aren't going to waste our readers time with the Trumpster and his beef with the NFL. We will state one thing and one thing only, the United States is a great country and it has provided us with the framework to ensure equality and natural rights, which unfortunately are things we must continually fight for. No matter one's opinion we feel that without history there can be no future, thus we must all learn from our pasts and be more tolerant and succeed where others have failed.

Ok now to where we stand technically via our charts. We will lead off with US Treasuries considering the FOMC week we just had, in particular the 2 year US treasury yield chart, as you can see it's taken nearly a decade to get back to 1.45%!

When looking at the 10yr in a more shorter time frame, after the initial run up in yields we can see them slowly rolling back down:

Moving to the currencies, both the Yen and the Euro seem to have been negatively affected by the stronger FED rhetoric as some profit taking seems to have hit the complex. First up the Yen which failed near 9400 and is now near critical 8947 support:

The Euro is once again under that important 11945 level and looks poised for further downside probes:

Gold and Silver were sold as well as both sit right at Vwap supports:

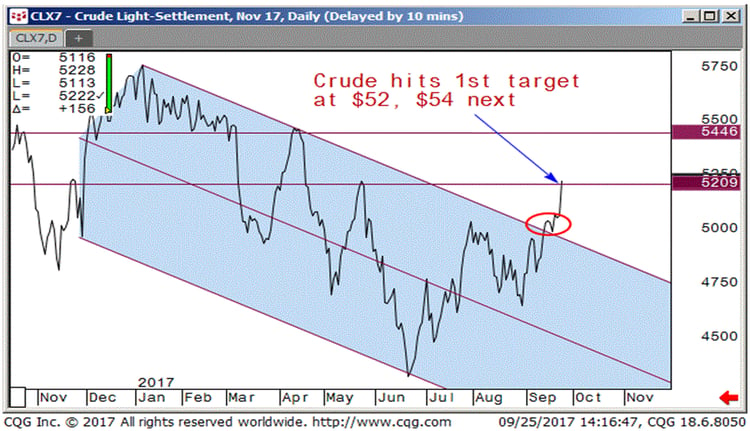

Keeping up with the positive correlation is the dollar and crude oil as crude oil pushed higher reaching our target area of $52 looking for a higher push to the all important $54.50 area:

Onward to equities and leading off with the laggard Nasdaq future where the 5911 level did not put up much of a fight, but rather almost acted like a catalyst for more downside, as a bearish wedge pattern has formed:

The SP500 future is desperately trying to hold the 2500 line, but we suspect a break below 2478 would prove to be quite damaging:

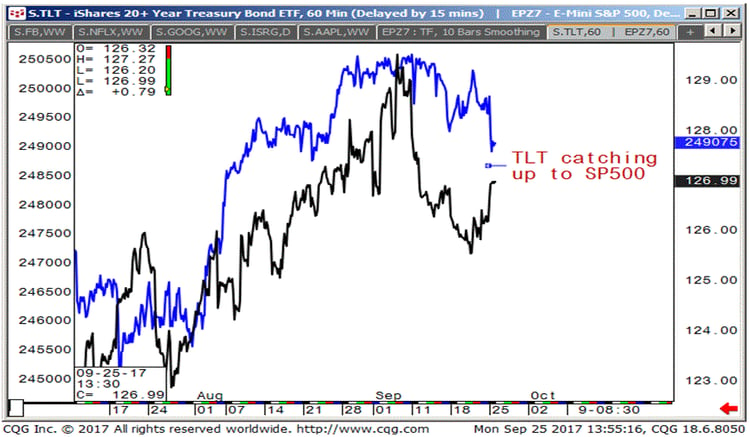

When we compare the SP500 to the TLT ETF in our analog chart, you can see how they are once again converging as the spread is narrowing, perhaps a more fundamental shift is in order but too early to tell:

Apple looks downright terrible and we suspect Peak Apple will start to gain traction below $137:

As for Amazon, we have been showing this chart since the July high and we have to say $940 seems poised to break and if it does another 10% downside is not out of the question. A few letters back we talked about how the Whole Foods acquisition might be a game changer, well it may seem so in more ways than one and not in the way most expected!

Hey let's not forget good old Facebook/Instagram (we included Instagram, seems more relevant), anyhow a 5% wack to start the week, ugh!

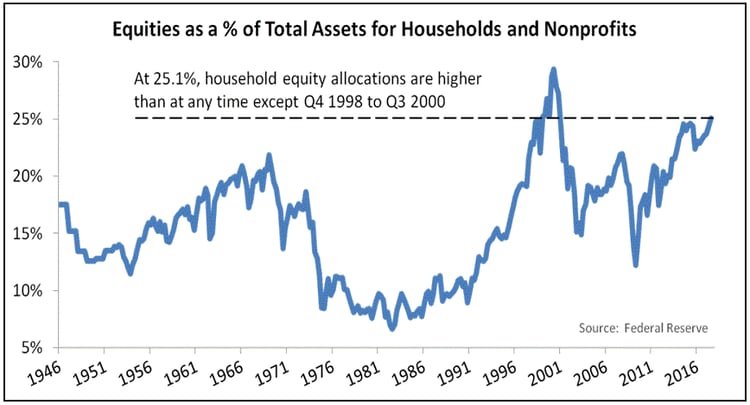

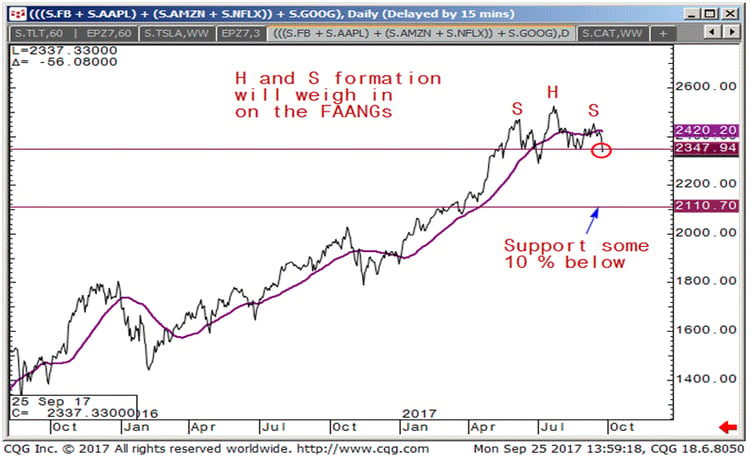

Our last chart is a doozy! Our coveted FAANGs, as we have stated in our previous letters, the big guns have been offloading some tech risk and it continues. Retail participation and margin levels are near all time highs, so it's no wonder to us this sector continues to roll. First let's look at that retail equity participation shall we:

Then again, we all knew once QE was implemented, that the wealthy asset holders would be by far the largest beneficiaries and obviously they were and its why the equity markets have exhibited near linear price growth as more and more buying begets, well, more and more buying. When global monetary policy is mired in constant asset purchases and interest rates are pegged near zero and sometimes even negative, this shouldn't be much of a surprise. Ok so now we got that retail is once again, all in, let's look at the our FAANGs chart, better technicians than us might be able to confirm this H&S top, but we know one thing 2347 is YUUGGE!

In conclusion we hope you enjoyed this lengthy rendition. As always we try to keep you a step above the rest in the only way we know how, buy filtering data and analyzing in ways that others do not. We try less to formulate and shape your opinion and more so try to stimulate your mind to cognitively think for itself. As always we leave you with the weekly settles and we can assure you, things will continue to get more and more interesting as the FED tries to pull back the reigns, nothing stays constant, this we are sure of. So stay tuned and stick with us, we have your back, Cheers!

Finally, we will decidedly end our notes with our reaffirmation of the growing need for alternative strategies. We would like to think that our alternative view on markets is consistent with our preference for alternative risk and alpha driven strategies. Alternatives offer the investor a unique opportunity at non correlated returns and overall risk diversification. We believe combining traditional strategies with an alternative solution gives an investor a well-rounded approach to managing their long term portfolio. With the growing concentration of risk involved in passive index funds, with newly created artificial intelligence led investing and overall market illiquidity in times of market stress, alternatives can offset some of these risks.

It is our goal to keep you abreast of all the growing market risks as well as keep you aligned with potential alternative strategies to combat such risks. We hope you stay the course with us, ask more questions and become accustomed to looking at the markets from the same scope we do. Feel free to point out any inconsistencies, any questions that relate to the topics we talk about or even suggest certain markets that you may want more color upon.

___________________________________________________________________________________

Capital Trading Group, LLLP ("CTG") is an investment firm that believes safety and trust are the two most sought after attributes among investors and money managers alike. For over 30 years we have built our business and reputation in efforts to mitigate risk through diversification. We forge long-term relationships with both investors and money managers otherwise known as Commodity Trading Advisors (CTAs).

We are a firm with an important distinction: It is our belief that building strong relationships require more than offering a well-rounded set of investment vehicles; a first-hand understanding of the instruments and the organization behind those instruments is needed as well.

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

This newsletter is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete. It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.