January 24, 2018

Before we get to the markets, we have to talk about something that concerns us. This week the government failed to gather enough senate votes to pass a budget resolution. We have been down this path before and it is just further testament to the ineptitude of those in congress to put the people first and their political agendas aside. We can’t say that we are the least bit surprised. What you may not know is the larger on going operation sweep to put to justice the bad actors responsible for the massive collusion of government agencies vs the then president nominee and now president elect Trump. Not only that, but there are massive implications for Hillary Clinton, the DNC and a firm called FusionGPS that compiled the so called “Trump Dossier.”

We feel there will be more implicating memos in the coming days and weeks and that a massive cover up is going to blow wide open. We can’t opine as to the effects it will have on domestic markets, but we want our readers to know that the domestic political front, has yet to negatively influence equity markets but we would be remised if we didn’t forewarn our readers that things are beginning to heat up. It is hard to distinguish the facts and the fakes these days, but we will do our best to decipher the news feeds and bring you bonafide data.

Anyway and another important and mostly overlooked by the media news outlets is the Senate passed the FISA Section 702 Reauthorization which allows the US government to collect communications. Some will ask why that is even a big deal. Well it basically is stating that anything digital that is out there and relayed through the internet, the cell phone etc, can and will be monitored. This is what Snowden unleashed to the public but the 702 specifically targets foreigners, but it has been well documented that US citizens are naturally caught in the net as well, and this has huge civil liberties conflicts, one we should all keep a lawful eye upon.

We had the honor of attending the Annual Chicago Economic Forum hosted by the Executives Club of Chicago. We were completely amazed by the massive attendance, wall to wall and as some were overheard saying they have never seen it more packed. Dr. Bob Froehlich, Dr. Art Laffer and the venerable Diane Swonk were the noted speakers and Terry Savage the host of the last 38 years rounded out the panel.

Mrs. Swonk took a more conservative approach to the outlook this year using Prince and party like its 1999 analogies, but with considerable more leverage now. She noted that we may not have the tools to deal with the next crisis; she was the lowest estimate of this year’s GDP, looking for a 2.7 print. She expected a 3.4% 10yr rate and 4 rate hikes for 2018.

Dr. Bob was purely more optimistic calling for a +4% GDP a 10yr rate of 2.7% and a Dow over 30k. He did shed some light on something we never heard of before, but will now put on our radar, that is DOTA. We were like what the hell is he talking about. Well we believe DOTA stands for “Defense of the Ancients.” It’s a multiplayer online battle arena mod for the video game Warcraft. The reason Dr. Bob brought this up is because a new blue ocean has been created. A whole new industry is rising and has the power of the millennials behind it. The prize purse for the 2017 tournament was near $25 million! We couldn’t believe it, but if you want to see the mania for yourself here is a good place to start here Now we know some of our readers are like WTF, but hey those of us with younger kids, this is truly a force to be reckoned with and not everyone is focused on traditional sports. This is the real deal and we are glad Dr. Bob brought this up.

As for Dr. Laffer, we truly enjoyed his down to earth yet forthright manner. He seemed to be in quite contrast with the more liberal Diane Swonk and his conservative yet abrasive approach was met with a kind and collegial manner one would expect at a high powered presentation like this. He did hit home on a few harsh comments about his old home town Chicago, stating things like you have to live with the choices when you elect certain people to office…What are you people thinking electing people like this and expecting anything to change, he said. One thing we liked was his quote saying, “Economics is about incentives, we don’t want to look at making the rich people poorer, but rather making poor people richer.” He seemed to really like JFK and he quoted him too saying “No American is made better off by pulling another American down.” We have never heard this quote before, but we will certainly put it in our arsenal as it truly hits at and resonates what it truly means to doing what is right.

We are all too often divided by a media that paints this parallels of black vs white, rich vs poor, that’s all BS, what it boils down to is that we need to realize that in a civil society we must not only be responsible for ourselves, but we must also have some responsibility to our fellow citizens. Dr. Laffer didn’t make any predictions, but he felt that America has a chance to truly prosper but it will take the right amount of fiscal policy with the right monetary policy, one we whole heartedly agree.

In other news:

Netflix explodes on slight earnings beat but really on the 8.4 million subscribers added in Q4. Despite the stock rising to nearly $260 all is not as rosy as free cash flow continues to fall as full year FCF was -$2.0 billion. Hey we like their content but it comes at heavy price of $17 billion in accrued content commitments. Their content is better than most and we can attest to the efficacy, with shows like Stranger Things, Orange is the New Black, Ozark, Master of None, Mindhunter and the list goes on.

Apple Inc. is going to pay a onetime tax of $38 billion on overseas cash holdings. Estimates are for Apple to to contribute nearly $350 billion to the U.S. economy over the next 5 years. We feel these are bold assumptions considering their reliance on the Iphone, their increasing debt issuance and overall economic prospects. What we have yet to really figure out with overseas repatriation is how much is really there? Can’t corps just use exotic swaps to transfer currency risk to other foreign corps doing business in the U.S.? We know most aren’t versed in this subject, but it certainly makes sense for these large companies to do such trades and circumvent all this repatriation and certainly avoid paying any tax whatsoever, perhaps that’s a topic for another day.

AmazonGo is live after a year of beta testing in Seattle this week. We believe it’s taking the “grab and go” to a whole other level and will be interesting to see how it fares in the coming months and how aggressive Amazon is with the roll out. As the stock is priced for perfection we are very interested to see if rates continue to rise and if the economy does indeed slow how all this will shake out. We must say the other retailers are certainly on notice and we expect the Walmart/Amazon battle to continue. Obviously this type of store is not for the basic commoner and will certainly be situated in more upper class areas, so this limitation may hinder its long term prospects in our opinion.

We read an interesting piece in Chicago Crain’s magazine this week about Sam Zell’s REIT. Mr. Zell continues to sell off properties and build a considerable cash war chest. His portfolio of holdings are down to just 20 properties from 156 just three years ago. We aren’t sure if this should be taken as a loss in confidence, but considering Mr. Zell’s acumen for sniffing out things, we would bet that higher interest rates are part of his equation to relinquish the majority of his holdings and not to mention prospects of overheating cap rates. We respect the man, so we take this as more than just conservatism.

China reported its largest U.S. surplus last week which rose 10% to nearly $276 billion. Trump has vowed to take action, but in reality what can the U.S. truly do? You can’t have globalization without labor arbitrage and you can’t go full tariff and protectionist and risk isolationism. The strange things about tariffs is that U.S. based manufacturers will merely use it as an excuse to raise prices toward the tariff rate to increase margins, which is what’s being seen in the U.S. lumber markets with tariffs being put onto Canadian lumber as well.

Walmart was touted in the news as it decided to move starting hourly pay to $11. However the flip side to that story is the fact that they plan to cut 10k jobs and close 10% of its Sam’s Club warehouse stores, so give a little, but takeaway just a little bit more.

Global banking fixed income trading revenues were hit across the board. We can’t say we are the least bit surprised given FDodd restrictions, passive investing and nascent volatility but all of the big 4 banks (JPM,CITI,GS,BofA) all reported substantial declines of 34%,18%,50% and 13% respectively in the 4th quarter. Perhaps the shrinking yield curve and higher rates will improve their trading gains in Q1 but we will continue to blame central banks for the lack of volatility and the near linear climb in equity overvaluations, which puts a hindrance in all if not everyone’s trading activity.

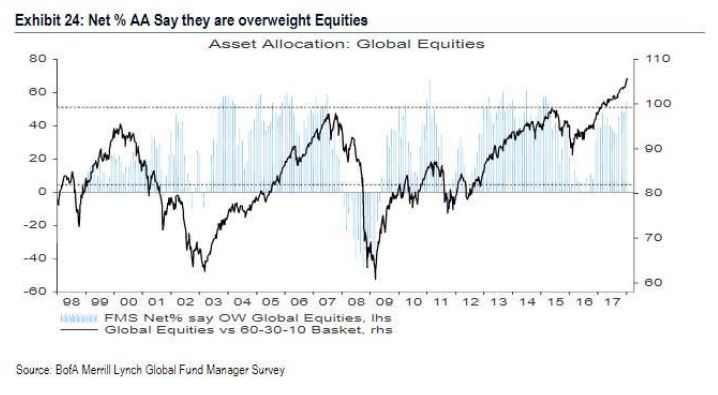

Considering fixed income trading is down, maybe it’s because everyone has finally drunk the kool-aid and realized the only game in town are equities:

Some will look at this chart from a purely fundamental perspective and think, wow this is so overbought it is an easy sale…yet in reality if you look at it from a prime, primped and pumped central bank fiat bonanza perspective from the last 9 years, one can simply make the case that we are merely above the prior peak and we have central banks continuing to print trillions each year. So with that crutch and support in mind, perhaps we should expand the chart a bit more and realize anything is possible.

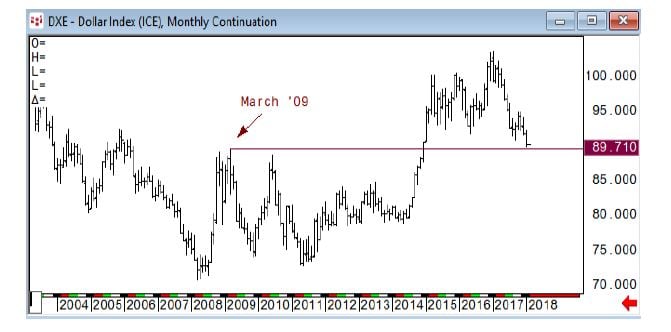

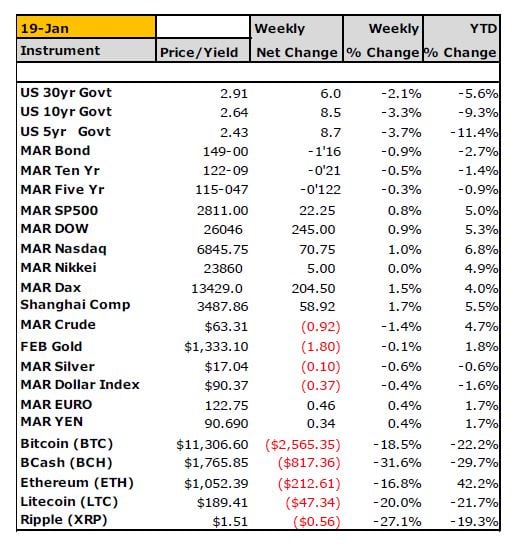

As far as the financial markets are concerned the trends are still intact. The global equity markets continue to rise as the U.S. markets were all up nearly 1% on the week. The U.S. bond market continues to fall as interest rates continue to rise with the U.S. 10yr rate ending the week at 2.64%. We feel and have stated before that 2.67% is our line in the sand there and we will expect it to be defended. This should also put the 30yr right near 2.95%. The 2yr yield is just above the 2.05% level the highest in some 10 years. We would expect rise in yields to attract some long term value players as comparison dividend yields on the SP500 are sub 2%. Something has to give we suspect, either the SP price falls and raises the yield above the 2yr rate or the Fed has overstepped here and will consider a slower paced path. We are a bit perplexed at their situation and we don’t see how they get themselves out of this tight rope scenario. With the yield curves near decade lows, we can’t help but notice the trade weighted dollar is near 2008 levels as well shown here:

We feel that the dollar can continue its slide and the move may usher in trend followers below that 89 level. The repercussions of a hawkish FED a flat yield curve and massive amounts of tax stimulus and Treasury debt will punish $$'s and will cause a hyperinflationary nominal asset price increase, i.e. SP500 well over 3000. Better hedge your $$ exposure though…

Japanese purchases of U.S. Treasuries have also slowed because of funding costs which have surged lately and where the pickup in yield doesn’t adequately compensate their domestic investor. Will this portend to a higher Yen/weaker dollar? Will yields begin to rise in Japan? Perhaps this is why the U.S. bond market has had a tough time lately, double the net Treasury issuance this year with waning foreign demand and we will need some domestic or European counterparts to do the heavy lifting. This is why the FED is truly in a tough position, they know the monster they have created, yet once Pandora’s Box was opened, there was never truly an exit plan.

We will now turn it over to the segment we know as:

CryptoCorner

- China’s mining giant Bitmain Technologies is considering another expansion - this time in Canada’s Quebec province

- Kraken, the fifth-largest cryptocurrency exchange, has resumed service after scheduled maintenance that was supposed to take two hours but instead took two days

- Maersk and IBM are working toward applying blockchain technology to create a more efficient and secure platform for organizing global trade. The companies have already tested the platform and we expect wider adoption as time move on

- Japan’s largest Bitcoin exchange BitFlyer launches in Europe, BitFlyer operates in Tokyo which houses 30% of the global bitcoin trading and will now be the only licensed European exchange offering cross-border trading with Japan

- The Corbett Report put out a great piece and must see for our readers, called the “Bitcoin Psyop” it is really informative

- Nassim Taleb this week said Bitcoin may fail in its present form but the framework is now open and the future of decentralization is upon us. (As these govt’s continue to pound more debt down our threats, their system is failing but allowing for a very few to control the lives of everyone else. Point being, if the commoner was smart they would adhere to abandoning the current system and adopting a decentralized one where the stakeholders (users) control the fate not some (3rd party entity)

- New Bitcoin addresses continue to average 2 million per week, this is the kind of massive migration that will slowly add to the stability of the Bitcoin core blockchain. Adoption continues to be steady and the people are continuing to advance and adhere

- The largest Bitcoin wallet was steady and the next 2 in line both added over 6k BTC to their holdings putting their total BTC owned at 179203,150808 and 117170 respectively. As large hodlers continue to acquire BTC

- South Korea continues its regulatory reach as it now is targeting taxing exchanges and mandating data collection including customer bank account data

- South Korea seems to be following the Chinese authorities abilities to crack down on the Crypto space, but in reality the decentralized nature will continue unabated and the space will continue to move towards countries with a more proCrypto agenda -More than 100k South Korea residents have signed petitions asking the government there to step back from any plans to close the country's cryptocurrency exchanges

- CFTC has recently created a Division of Enforcement Virtual Currency Task Force

- SEC Division of Investment Management (the "Division") advised funds that are investing significantly in cryptocurrency not to seek to register their securities or otherwise to sell securities in a public offering

- KodakCoin Will Trade On Overstock's New Cryptocurrency Exchange

- The EpochTimes had a great must see interview with Trace Mayer, he paints a very realistic approach to Bitcoin and blockchain

The ongoing government outreach has put a cap on further price appreciation, yet we aren’t too clear as to the effectiveness or the intelligence behind their rash and somewhat incomprehensible rationale. What it says to us is that the governments truly underestimated the sector and are now trying to play catch up and will no doubt continue to paint a nefarious claim unto any player in the space. The people will need to stand up and realize that the governments are purely overstepping their reach and will continue to do so unless the community of private investors changes their course. At what point do we say that we know what’s best for us and we don’t need a government to protect us from ourselves. It should be rather eye opening to the investor community that governments are so quick to make resolutions that they completely disregard any private stakeholder input. This is a sign of a wider global epidemic of government authoritarian style control, which seems to operate without bounds.

Thank you. We hope you have a good week and we hope you continue to stay the course with us. As always, we leave you with the weekly settles below. The Crypto space continues to be hampered by government regulation as a pullback in most if not all Crypto currencies was seen. No doubt the sector has come a long way in a relative short time and lower probes and consolidation are a technical and fundamental nature of any market. Cheers!

Finally, we will decidedly end our notes with our reaffirmation of the growing need for alternative strategies. We would like to think that our alternative view on markets is consistent with our preference for alternative risk and alpha driven strategies. Alternatives offer the investor a unique opportunity at non correlated returns and overall risk diversification. We believe combining traditional strategies with an alternative solution gives an investor a well-rounded approach to managing their long term portfolio. With the growing concentration of risk involved in passive index funds, with newly created artificial intelligence led investing and overall market illiquidity in times of market stress, alternatives can offset some of these risks.

It is our goal to keep you abreast of all the growing market risks as well as keep you aligned with potential alternative strategies to combat such risks. We hope you stay the course with us, ask more questions and become accustomed to looking at the markets from the same scope we do. Feel free to point out any inconsistencies, any questions that relate to the topics we talk about or even suggest certain markets that you may want more color upon.

____________________________________________________________________________________

Capital Trading Group, LLLP ("CTG") is an investment firm that believes safety and trust are the two most sought after attributes among investors and money managers alike. For over 30 years we have built our business and reputation in efforts to mitigate risk through diversification. We forge long-term relationships with both investors and money managers otherwise known as Commodity Trading Advisors (CTAs).

We are a firm with an important distinction: It is our belief that building strong relationships require more than offering a well-rounded set of investment vehicles; a first-hand understanding of the instruments and the organization behind those instruments is needed as well.

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

This newsletter is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete. It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.